Research / Validation / Deployment

Systematic alpha,

engineered to operate

while you don't.

Nine broker-validated systems across indices, FX and crypto — one controlled institutional execution layer that never sleeps and never improvises.

Scroll to enter the system

Move from thesis to system architecture, then into the live portfolio and validation stack.

Operating Thesis

Portfolio logic before platform theatrics.

Session Coverage

Tokyo -> London -> New York

System Stack

7 independent models

PF

0.00

DD

0.0%

Trades

695+

System Snapshot

The thesis should be visible before the first scroll.

Validated EAs

09

Survivors of 113 candidates

Backtests

199

Engine + broker. Proven twice.

Rejection Rate

92%

104 strategies killed

OOS Decay

1.04

Out-of-sample. Zero degradation.

Thesis 01

Validated through rejection: 104 of 113 strategies were killed.

Thesis 02

Two-layer proof: research engine plus broker-data Strategy Tester.

Thesis 03

Audited independently — defects published, not hidden.

Thesis 04

Out-of-sample evidence before capital, not after.

00 / The System

Four layers. Zero improvisation.

Hover to open each layer of the stack.

Validation Funnel

113 ideas in. Nine systems out.

The edge is not only in what survives — it is in what gets eliminated. Every strategy faces the research engine, then the broker's own bars, then full-history stress.

Detail 01

113 strategies catalogued from 28 families

Detail 02

199 backtests across two independent layers

Detail 03

92% rejection rate before capital allocation

Highlight metric

104

Execution Forensics

Bugs are hunted, not hidden

An audit traced dead strategies to a midnight session-break defect: orders fired at the daily bar open and died with 'market closed'. The fix resurrected two systems from zero trades.

Detail 01

Order-retry layer added without touching strategy logic

Detail 02

Two EAs went from 0 trades to fully measurable

Detail 03

Findings published in the remediation log

Highlight metric

02

Out-of-Sample Proof

The anchor passed the only test that matters

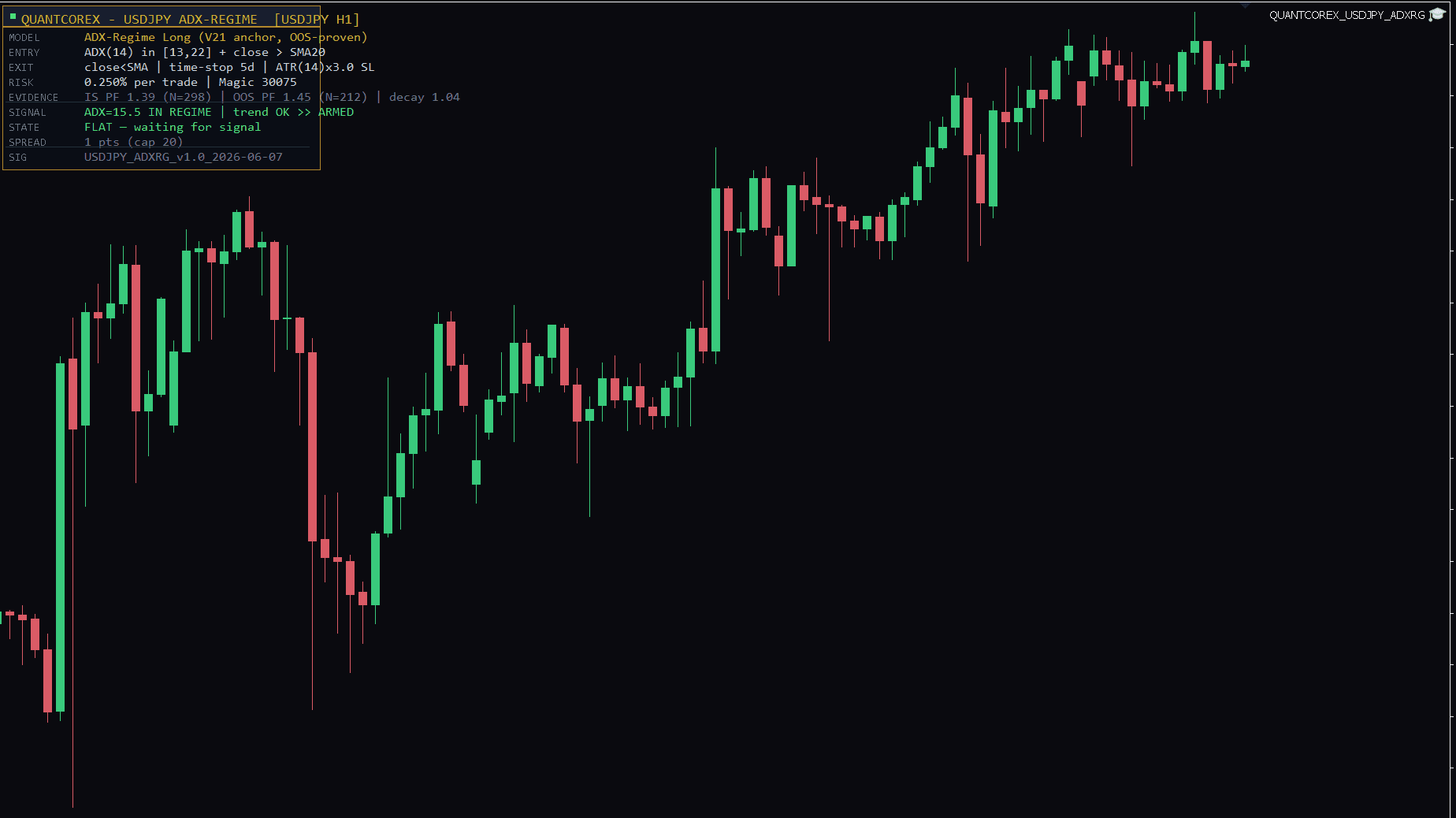

USDJPY ADX-Regime H1: 298 in-sample trades, then 212 out-of-sample trades on unseen data. The out-of-sample profit factor came back HIGHER than in-sample.

Detail 01

IS PF 1.39 (2023-04 to 2024-12)

Detail 02

OOS PF 1.45 (2025-01 to 2026-04)

Detail 03

692 trades on the full 2022+ window, PF 1.63

Highlight metric

1.04

Risk Engine

Cluster risk as architecture

Correlated dip-buyers share one position budget enforced in code. Three EAs buying the same S&P dip is one bet, not three — the system treats it that way.

Detail 01

Max 2 concurrent positions per strategy cluster

Detail 02

0.125% base risk per trade, halved on probation systems

Detail 03

Worst-case simultaneous exposure: 0.875% of equity

Highlight metric

0.875%

01 / The Problem

Humans break before markets do.

Discipline fails exactly when it is needed most. So we removed it from the loop.

Session Sequence

Asia accumulates. London sweeps. New York distributes.

Asia

Accumulation

Range building before directional intent.

London

Manipulation

Liquidity sweep through the resting extremes.

New York

Distribution

Expansion away from the engineered sweep.

You can't monitor 7 instruments across 3 sessions.

You can't execute at 3am.

You can't remove emotion.

You can't keep decision quality constant under fatigue.

You can't rebalance risk across regimes with intuition alone.

02 / The Edge

Not one model. Nine proven systems.

Each engineered for one behaviour. Each forced to survive the broker's own data.

Systems

9

Distinct logic stacks for distinct regimes.

Families

5

Reversion, regime, breakout, sweep, momentum.

Risk Engine

1

Capital allocated as a coordinated system.

Coverage

24h

One mandate across the global liquidity clock.

03 / Anatomy of a Trade

Not a belief. A sequence.

Five live families. One chart each. This is what the machines actually trade.

RSI-2 Mean Reversion

Buys short-term panic above the 200-day average. Sells the bounce. Sixty-nine percent of the time, the market obliges.

04 / Validation

113 in. Five survive.

92% of everything we built was killed before touching capital.

ADX-regime D1

0 / 28 configs

DE40 reversion

PF 0.99 broker

UK100 IBS

PF 1.05 · 4.3y

TPS-3 standalone

100% = RSI-2

XAUUSD ×12

12 families dead

RSI-3 US500

PF 1.00 full

A research process that never rejects anything is a marketing process.

05 / Portfolio

The system view is the product.

Nine instruments. One risk engine.

Core Book PF

1.59

Deploy-Grade EAs

5 / 9

Worst-Case Risk

0.875%

USDJPY

ADX-Regime · H1

PF

1.41

Win Rate

28.8%

Risk

0.125%

Expectancy

0.29R

Avg R:R

3.49

Max DD

2.33%

510 closed trades / hover reveals system diagnostics

US500

RSI-2 Reversion

PF

2.92

Win Rate

69.4%

Risk

0.125%

Expectancy

0.59R

Avg R:R

1.29

Max DD

0.26%

36 closed trades / hover reveals system diagnostics

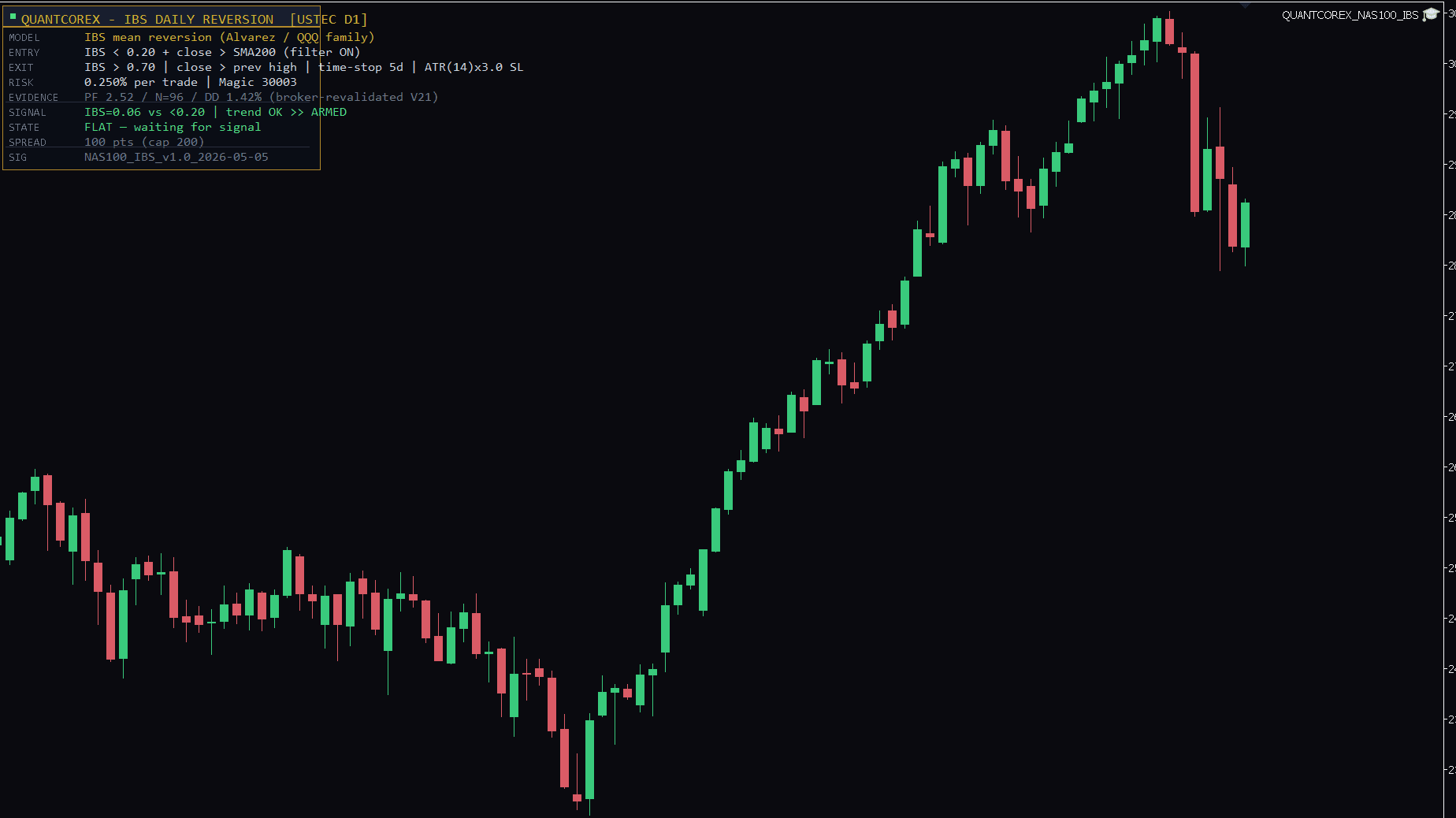

NAS100

IBS Daily Reversion

PF

2.52

Win Rate

74.0%

Risk

0.125%

Expectancy

0.40R

Avg R:R

0.89

Max DD

1.42%

96 closed trades / hover reveals system diagnostics

GBPUSD

RSI-2 Pullback · H4

PF

1.34

Win Rate

64.5%

Risk

0.125%

Expectancy

0.12R

Avg R:R

0.74

Max DD

1.56%

214 closed trades / hover reveals system diagnostics

NAS100

Donchian 30/15 Breakout

PF

1.93

Win Rate

52.2%

Risk

0.125%

Expectancy

0.44R

Avg R:R

1.77

Max DD

2.62%

23 closed trades / hover reveals system diagnostics

NAS100

RSI-3 Triple Bottom

PF

2.13

Win Rate

66.7%

Risk

0.125%

Expectancy

0.38R

Avg R:R

1.07

Max DD

1.51%

18 closed trades / hover reveals system diagnostics

NAS100

Composite-RSI

PF

1.70

Win Rate

62.5%

Risk

0.125%

Expectancy

0.26R

Avg R:R

1.02

Max DD

2.29%

40 closed trades / hover reveals system diagnostics

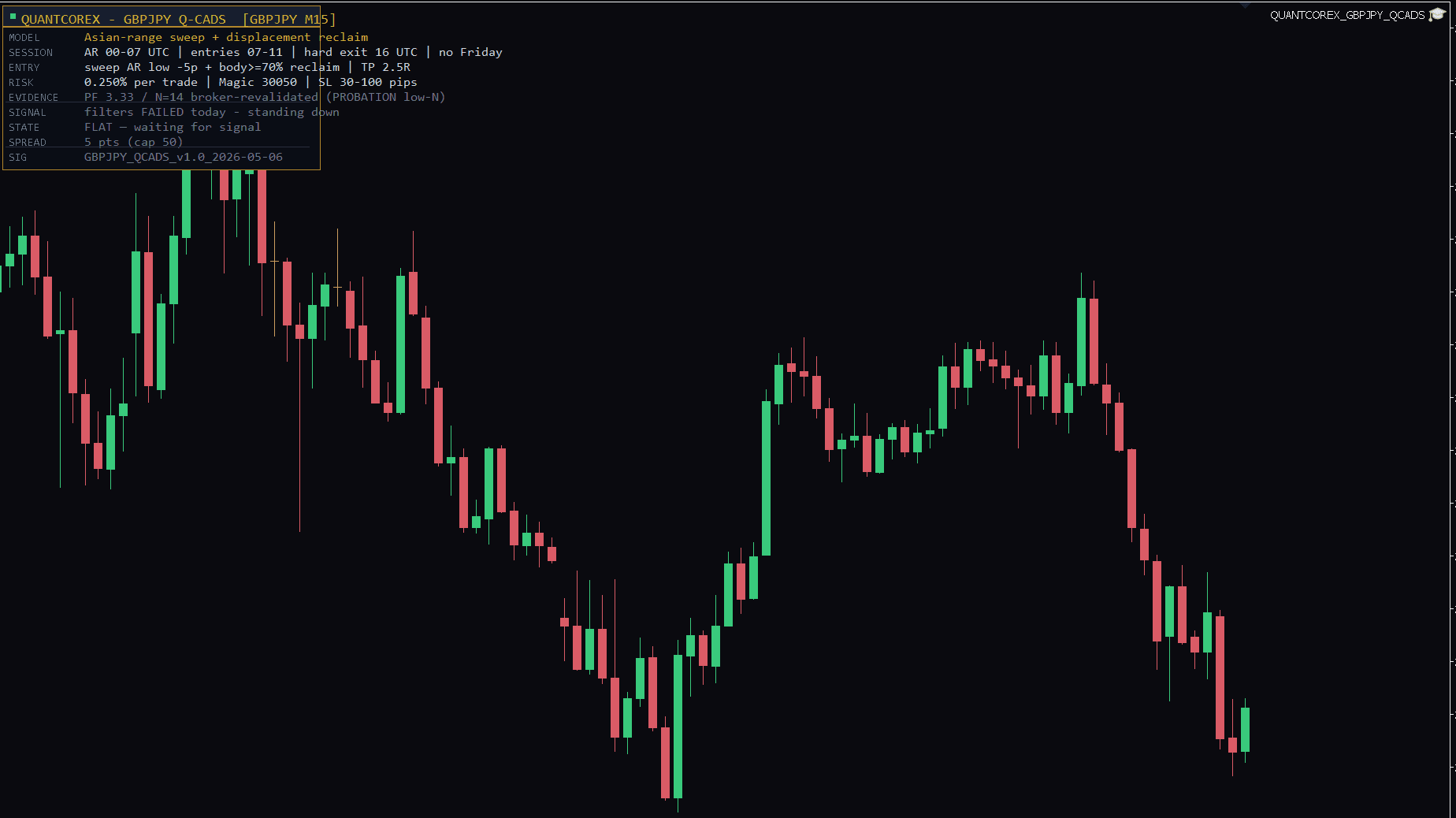

GBPJPY

Q-CADS Stat-Arb

PF

3.33

Win Rate

71.4%

Risk

0.075%

Expectancy

0.67R

Avg R:R

1.33

Max DD

0.68%

14 closed trades / hover reveals system diagnostics

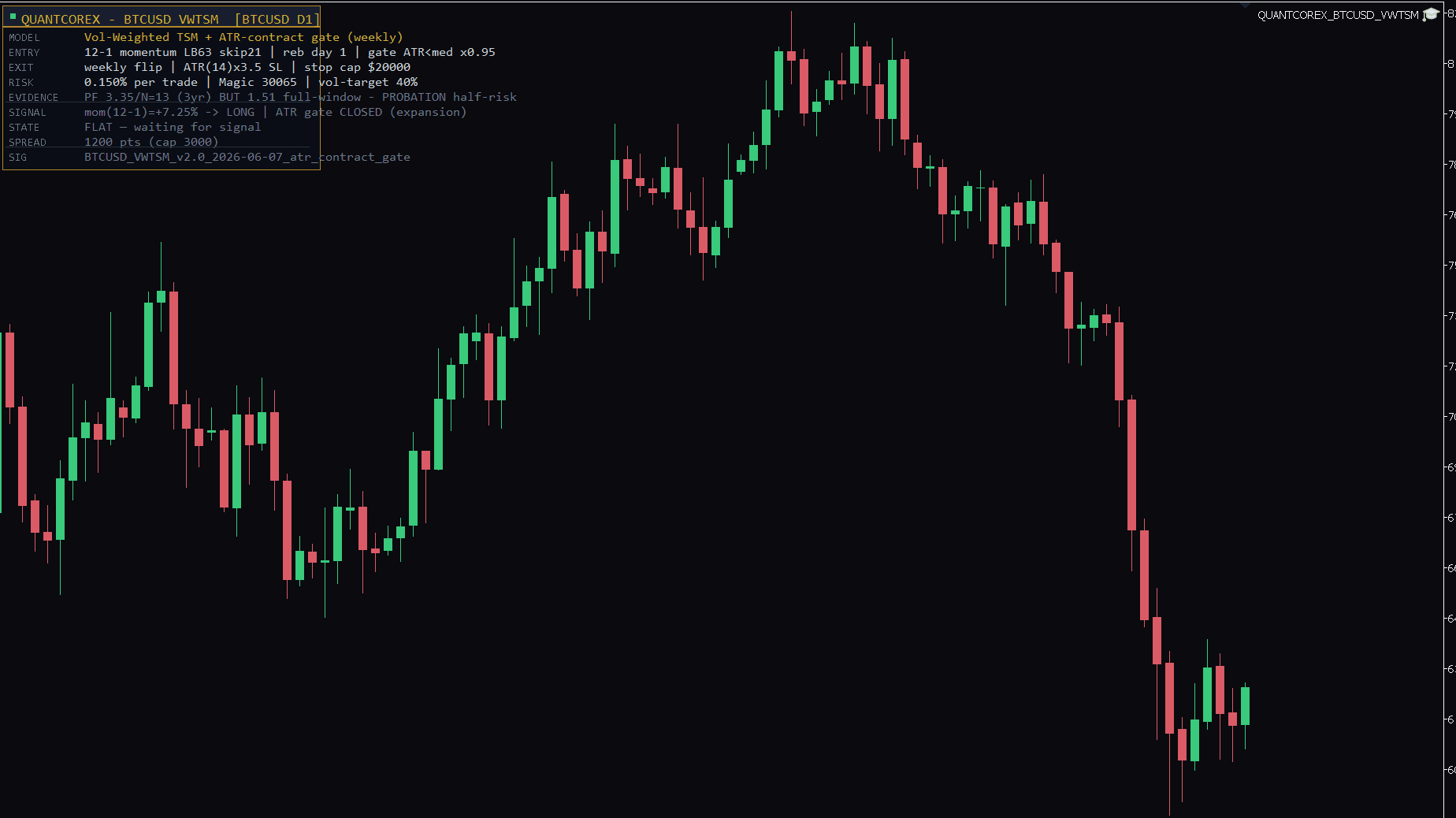

BTCUSD

VWTSM Momentum

PF

3.35

Win Rate

62.0%

Risk

0.075%

Expectancy

0.89R

Avg R:R

2.05

Max DD

4.76%

13 closed trades / hover reveals system diagnostics

06 / Risk

Survive first. Scale second.

Per trade. Per cluster. Per portfolio. Capped in code, not in promises.

Exposure Grid

0.25% per trade.

Never all-in.

Built to survive.

Session separation prevents the portfolio from unintentionally stacking the same risk expression into one market window. Capital is sized to absorb adverse periods without compromising the operating system.

07 / Live Deployment

Not a backtest. A terminal.

Captured live on the broker's MetaTrader 5 — each machine reporting its own model, evidence and state. Two armed. Two standing down. That is the discipline.

IC Markets demo · captured 11 Jun 2026 · panels render their own state — no retouching

08 / Performance

Consistency over spectacle.

4.3 years of broker data. Proven out-of-sample.

Portfolio Quality

0.00

Portfolio profit factor

Validated Window

4.3 Years

Full broker history 2022-2026, bear tail included

OOS Track

16 Months

USDJPY anchor: OOS PF 1.45 vs IS 1.39 — decay ratio 1.04

Max Core-EA DD

2.62%

Worst drawdown across the five deploy-grade systems

Equity Curve

Portfolio aggregate / 36 months

Out-of-Sample

Forward track after development window

09 / Position

Systematic alpha.

Engineered. Controlled. Repeatable.

Systematic

Engineered

Controlled

Repeatable

Access

For serious capital, the interface should be as disciplined as the system.

Request a private walkthrough, review the portfolio architecture, or open a direct conversation around deployment and allocation.